Stillfront: Right place, right time

As a fund manager, few things are more exciting to talk about than investment success stories. Naturally, not nearly all of our decisions since launching DNB Fund Nordic Small cap in December last year have been successes, but our Stillfront investment has so far deserved that label.

Stillfront is the largest position in the fund and has been so more or less throughout the year. The share is up by more than 130% YTD, and like any other investment success, our Stillfront story has been a perfect symbiosis of a (so far) correct investment thesis and a bunch of luck on top.

In investing, when talking about errors, we generally talk about being overly optimistic about the future development of a company. Absent of luck, these errors may lead to huge and disastrous investment mistakes where you buy and hold a stock, and it turns sour, eating into your principal. As a consequence, it is said that you learn more from your mistakes than from your successes. We tend to agree, but believe that some success stories (like Stillfront in this case) may give valuable insights as well: Attractive investment cases are often even better than you first dare to think, and as a portfolio manager underestimating successes is also a sin.

Attractive investment cases are often even better than you first dare to think, and as a portfolio manager underestimating successes is also a sin.

Stillfront at a glance

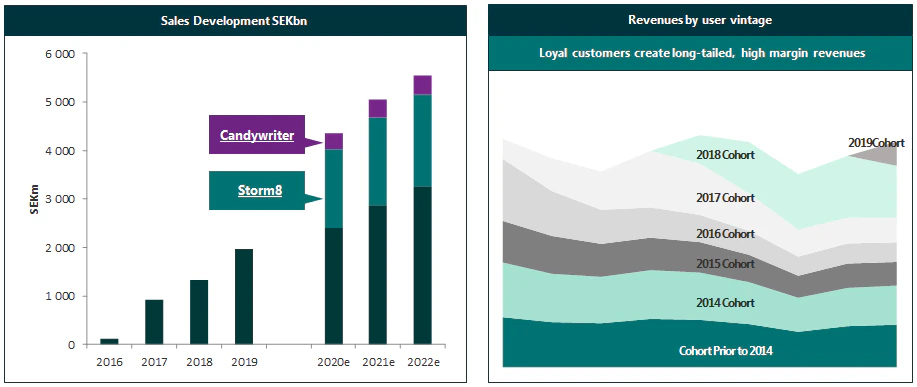

Stillfront is a group currently consisting of 14 game development studios headquartered in Sweden, focusing on free-to-play games for mobile, tablet and browser gaming, with in-app purchases accounting for close to all of the revenues. The group has traditionally focused on strategy and simulation games, but through large and transformative acquisitions on top of solid organic growth, Stillfront has become a more diversified player while also growing its top-line rapidly from just north of SEK 100m in 2016 to an estimated top line well above SEK 4bn in 2020 to match its market cap of close to SEK 30bn.

Stillfront: Sales development 2016A-2022e and Revenues by user vintage

Stillfront has now developed into an international, free-to-play powerhouse. Still, its impressive track record of growth has not compromised profitability, as operating margins have steadily increased to the mid-thirties alongside very satisfying cash generation.

As the company is not leaning on ad-revenues monetization among active users is the key factor. We believe the focal points of the game catalogue’s impressive profitability are the games’ remarkable longevity combined with its analytically driven approach to marketing and live ops. As several of the game titles are aimed at keeping players busy for years, successful live ops (in-game live events) and new content are crucial factors driving engagement and monetization. While each gaming studio runs rather independently inside the group, Stillfront runs a group-wide disciplined and data-driven approach to marketing and live ops. All marketing spend must have a net pay-back in six months or less, and live data on marketing responses enables Stillfront to rapidly optimize its user acquisition spend and allocate to the most profitable activities.

Hence, we believe Stillfront possess both a strong platform for new slam-dunk games, but maybe as important extremely strong capabilities in managing the tail of games that are out of the rapid growth phase. This, in turn, translates into a higher return on each dollar spent on user acquisition costs, driving long-term profitability.

Simple investment case, but stronger than initially anticipated

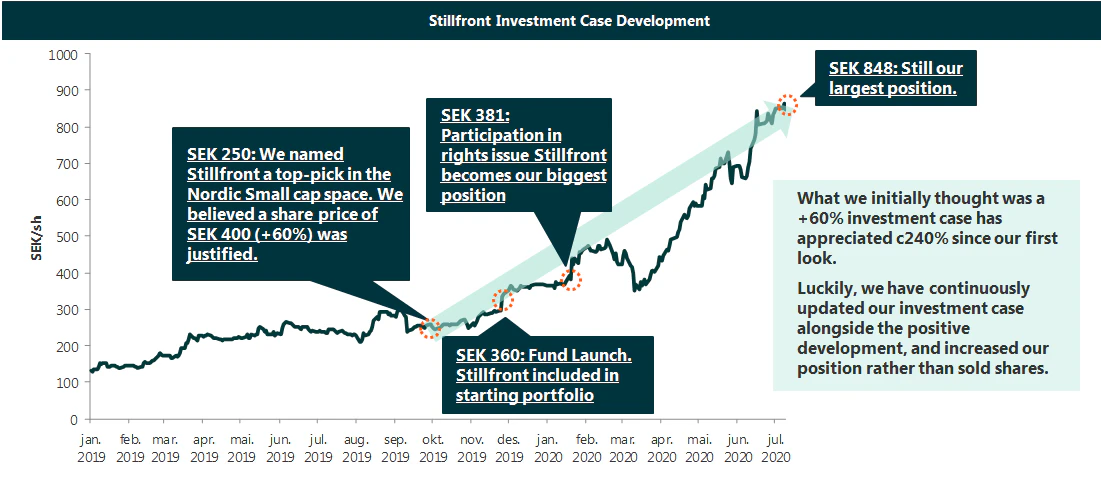

In the run-up to launching the fund last fall, we highlighted Stillfront as a top-pick in the Nordic small cap universe at different marketing events. Our investment thesis was quite simple: The stock market underestimated the longevity and hence earnings power of Stillfront’s portfolio of games, i.e., estimates were too pessimistic on both top line and margins.

At that point in time, the share price was around SEK 250, while we believed a share price around SEK 400 was justified.

We launched the fund in mid-December, and while the share price had appreciated to about SEK 360/sh, we still included a significant portion of Stillfront shares in our starting portfolio. In late January 2020, Stillfront carried through a rights issue at SEK 381/sh to fund the large acquisition of Storm8. We participated, and Stillfront became our top holding in the fund. It has stayed so throughout the year. At the time of writing, the share price is close to SEK 850.

The share price appreciation has been some 140% since the fund inception, and more than 130% YTD. Moreover, since we first looked at the investment case, it has appreciated by c240%. Safe to say, the share price has appreciated more than we first anticipated. And obviously, had we sold our shares at SEK 400 we would have missed out on a lot of fun. Luckily, we have constantly updated our investment thesis along the way, and along with stronger-than-expected development, we continuously increased our fair value estimate. Hence, we have been able to increase our position rather than to decrease it.

Sky is the limit?

While the share price appreciation over the past year has been extreme, we believe the future looks very bright for Stillfront and see further upside in the investment case from several facets.

Firstly we believe Stillfront will be able to achieve continued strong organic growth in a mobile gaming market that is growing underlying by some 10% per year.

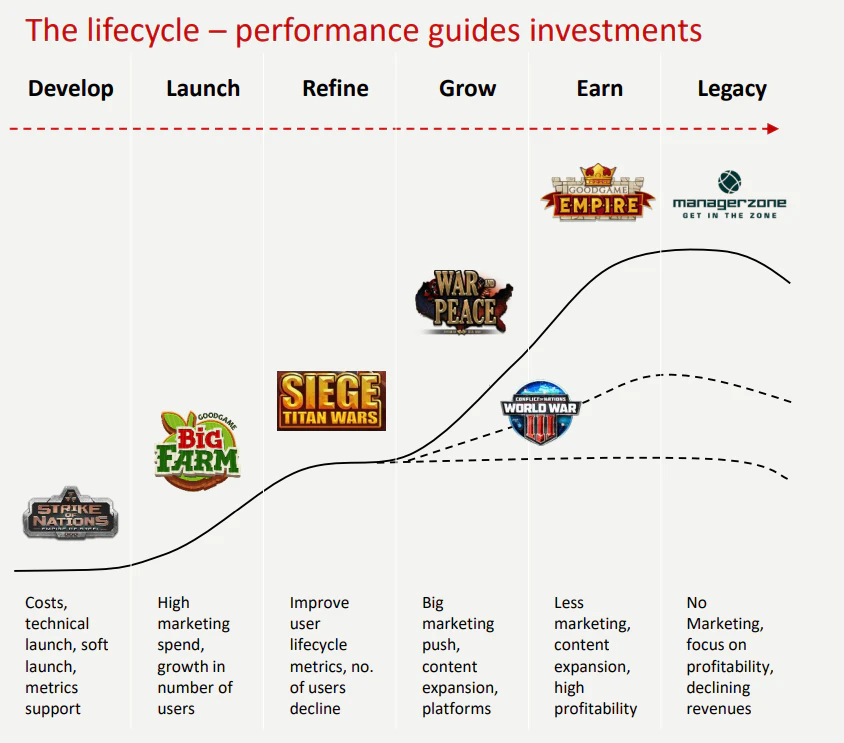

Secondly, we believe Stillfront will continue to be a consolidator in this very fragmented market, continuing its proven M&A track record. We believe Stillfront is able to achieve synergies both on costs (re-use of engines, leveraging existing assets) and on revenues (sharing of best-practice live ops execution, etc.). Acquisitions have historically been a significant catalyst for the share price, and we see no reason why this should cease.

Thirdly, we see a re-rating potential from increased diversification both through more titles, but primarily through penetrating new market pockets, for instance via genre mashups. An example is the acquisition of Strom8 in January this year, which specializes in a mashup between casual and puzzle gaming.

Lastly, we see scope for upped guidance as the company has already raced past the checkered flag on its 2022 targets.

Disclaimer: Nothing contained on this website constitutes investment advice, or other advice, nor is anything on this website a recommendation to invest in our Funds, any security, or any other instrument. The funds mentioned may not be available in the markets you represent. The information on this blog is posted solely on the basis of sharing insight to make our readers capable of making their own investment decisions. Should you have any queries about the investment funds or markets referred to on this website, you should contact your financial adviser.