Nordic high yield in the age of corona

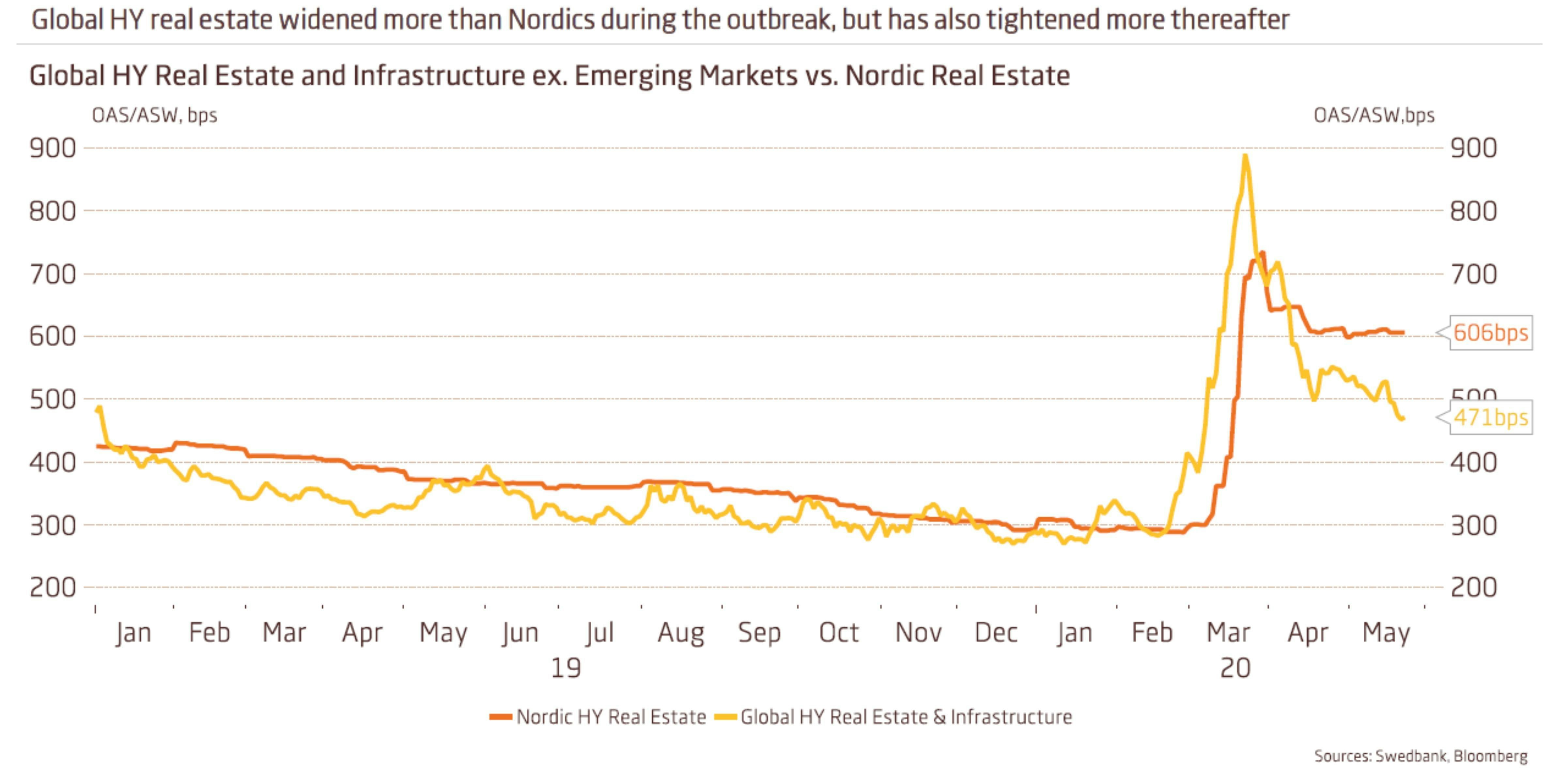

The extreme credit spread widening seen in March has since tightened but is lagging developments in the US and Europe

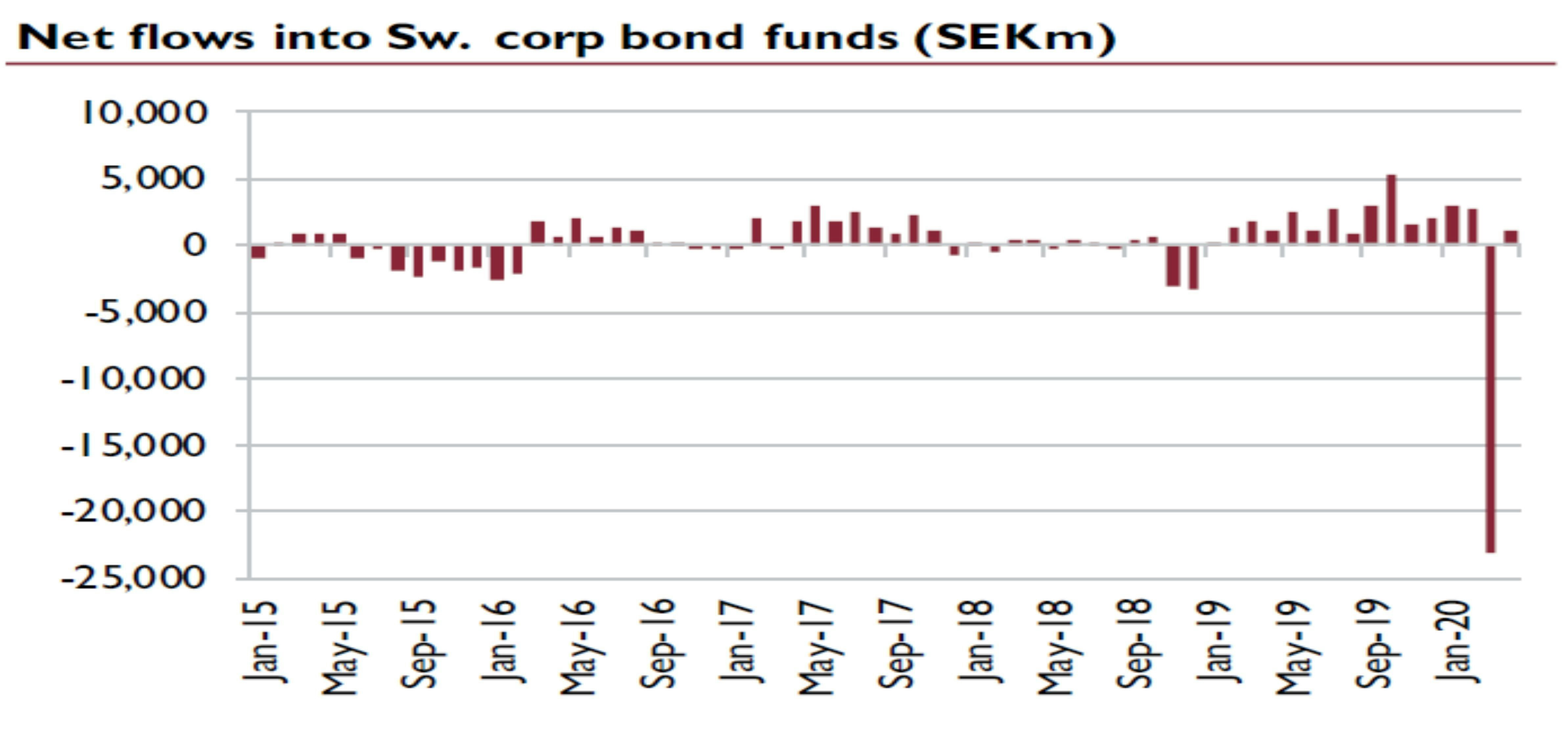

The spread widening in the Nordic high yield market was related to sharply increased global economic uncertainty and default risk, but also to some idiosyncratic factors such as excess selling in Norway to generate cash for currency hedges and massive outflow from Swedish credit funds and the resulting temporary closure/suspension of a number of the funds. Since late March spreads have tightened but the move has lagged developments in the US and European high yield markets.

Credit spreads in the Nordic high yield market exploded in March

March was a dramatic month in the Nordic high yield market. To some extent developments in the Nordic market mirrored what we saw in other high yield markets – massive spread widening based on a sudden deterioration in and increased uncertainty concerning the global growth outlook. This is only to be expected in a situation where authorities close down large parts of economic activity in most countries and there is uncertainty about the way back to a normally functioning economy. However, a couple of special factors in the Norwegian and Swedish sub-markets, respectively, led to a larger sell-off and a slower recovery in the Nordic market than elsewhere. These will be discussed in the following.

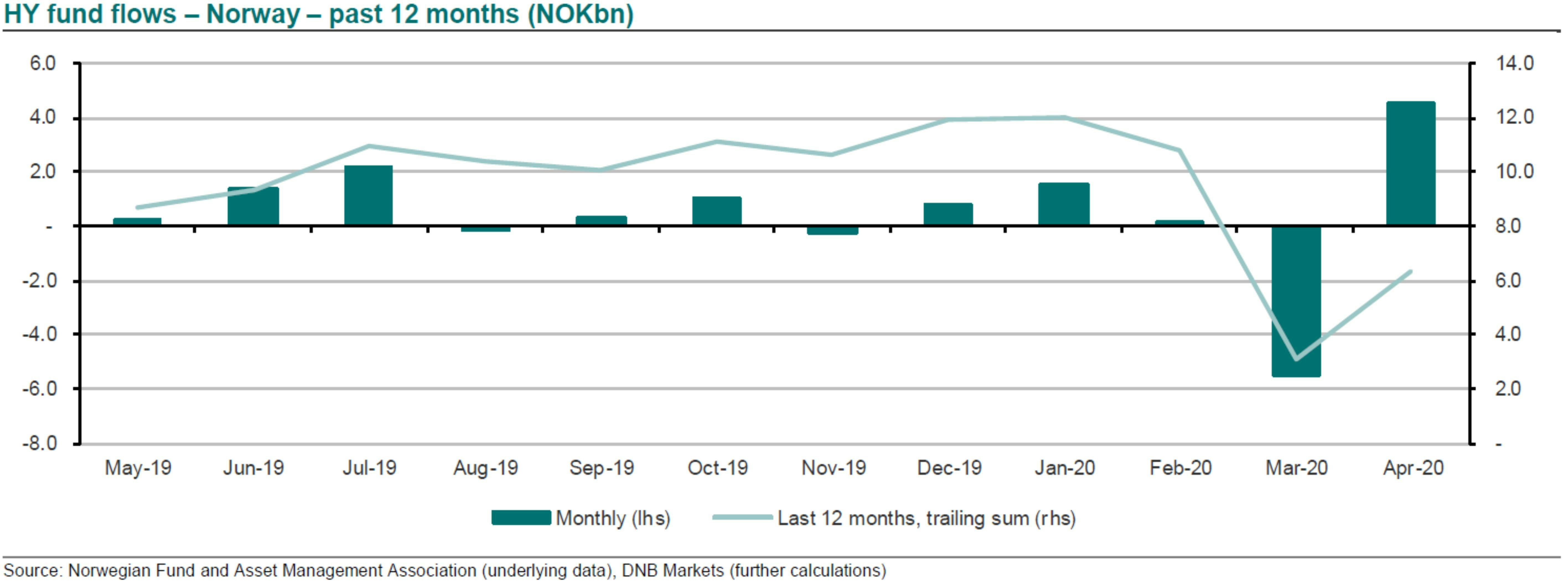

Norway – selling pressure from tanking NOK and currency hedging

Norwegian domiciled high yield funds have mainly Norwegian clients and are normally hedged to NOK. At the same time investments in the typical fund will be 25-30% in NOK as this percentage represents the overall NOK issuance in the Nordic market (the remainder of the issuance would be mainly in SEK, EUR and USD). Under the currency hedging contract arrangements the funds and their counterparties will exchange collateral (almost exclusively cash) on a daily basis as security for movements in the market value of currency hedges. When the NOK weakens the market value of investments in SEK, EUR and USD will increase and there will be a corresponding decrease in the market value of currency hedges necessitating a cash transfer from funds to counterparties.