Nordic High-Yield Bonds: Expect a Yield Premium

After a long time, the bond market is once again offering attractive returns. In addition, inflation is on the retreat in many countries. In other words, good conditions for an end to the rise in interest rates in the near future. Against this backdrop, Nordic high-yield bonds are an interesting option for institutional investors looking for a combination of attractive yield prospects, short duration and diversification effects.

The Nordic countries offer a unique investment landscape that combines diversity with stability. Norway and Sweden form the core, followed by Denmark, Finland and Iceland. Overall, these countries are characterised by high economic growth, robust per capita gross domestic product and political stability. Over the last 30 years, the Nordic countries have performed better than the rest of Europe in terms of GDP growth, but also better than the USA and Asia. At the same time, they have been more resistant to crises. In addition, there is an established governance structure in the companies.

This mix is ideal for listed companies to perform positively. Investors could and can benefit from this. It is no coincidence that the Nordic region has achieved impressive equity returns over the years. For example, the MSCI Nordic has significantly outperformed the MSCI World and the MSCI Europe over the last 20 years. But Nordic bonds are also interesting for investors. The high-yield segment (high-yield corporate bonds) is particularly worth mentioning here. There are several reasons for this.

Yield premium

The most important factor from an investor's point of view is certainly the attractive yield premium. On average, it is currently around 200 basis points higher than for high-yield bonds with comparable credit risk in the USA and the rest of Europe. One reason for the premium is that some companies on the Nordic high yield market do not have an official rating. This is seen as a flaw in the market and requires a corresponding premium. Added to this is the often relatively low volume of bonds issued. In relative terms, however, new launches in 2022 and 2023 were largely stable compared to other high-yield markets.

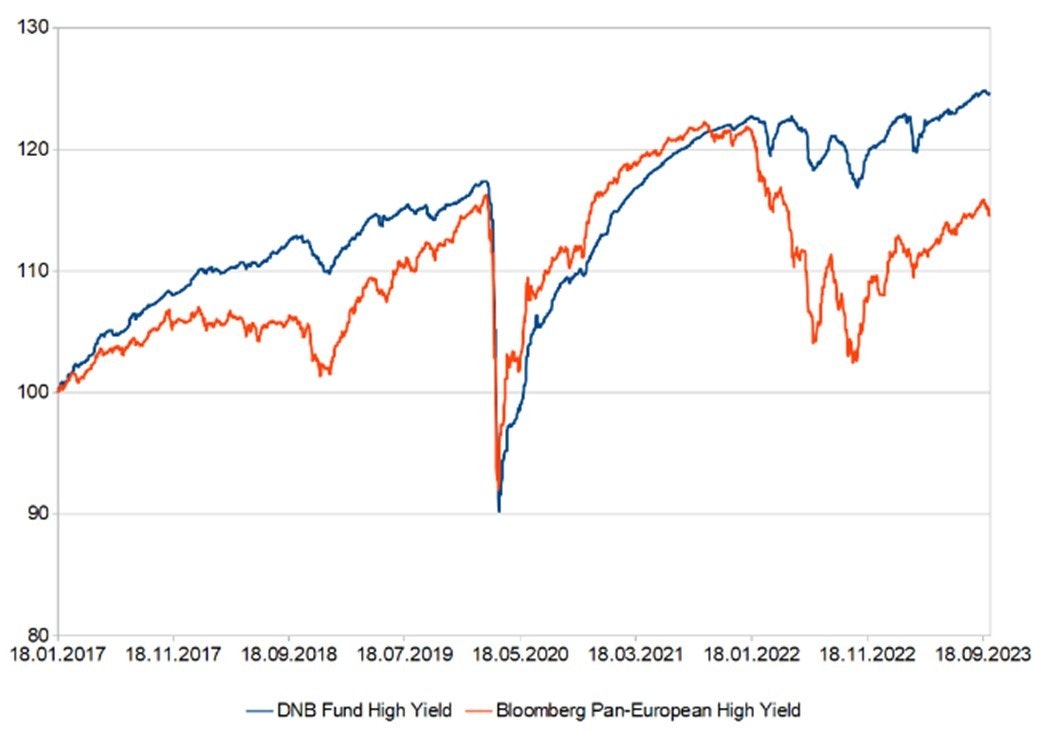

The DNB Fund High Yield outperformed the benchmark index. While the fund has increased by around 24% since January 2017, the Bloomberg Pan European High Yield Index has only increased by around 14% (as of 6 October 2023).

DNB Fund High Yield vs. Benchmark

Source: DNB; As of: 6 October 2023