Ce document est un support marketing. Les performances passées ne garantissent pas les rendements futurs. Les rendements peuvent être négatifs en raison de la baisse des valeurs de marché.

Les rendements futurs dépendront notamment de l’évolution des marchés, de la compétence du gestionnaire, du profil de risque du fonds et des coûts associés. Avant d’investir, il est recommandé aux clients de consulter les informations clés et le prospectus du fonds, qui contiennent des détails supplémentaires sur les caractéristiques et les coûts du fonds. Remarque : Investir dans le fonds signifie acquérir des parts du fonds, et non des investissements sous-jacents.

Rapport 2024 sur le potentiel d'énergie… | DNB Asset Management

Rapport 2024 sur le potentiel d'énergie renouvelable et les émissions évitées de DNB : Impact atteint à nouveau

Pour la sixième année consécutive, notre analyse montre que le portefeuille atteint un résultat net d'Émissions Évitée Positives (EEP). En d'autres termes, le portefeuille continue potentiellement à éviter plus d'émissions qu'il n'en émet.

PAE continues to improve amid evolving methodologies

Net PAE improved compared with last year, reflecting the continued strength of our investment approach in identifying climate-solutions providers. Scope 1 and Scope 2 emissions have generally declined since 2019, despite a temporary rise in 2023 and 2024 driven by changes in portfolio composition.

Scope 3 emissions increased year-on-year, but this stemmed largely from methodological changes applied by ISS-ESG rather than a deterioration in underlying company performance. As these figures are estimated, a degree of volatility is expected.

Overall, the results emphasise that directional insights matter more than absolute totals, particularly as methodologies, disclosure standards and portfolio weights continue to evolve.

Sector contributions shift, and energy saving takes the lead

For the first time, the Energy Saving sub-sector emerged as the largest contributor to total PAE. This was primarily driven by Signify, the global lighting company, which accounted for 21% of the portfolio’s absolute PAE.

Signify’s net PAE improved markedly, from –152.5 tCO₂e/EURm last year to –893.0 tCO₂e/EURm, supported by higher self-reported avoided emissions (240 MtCO₂e to 256 MtCO₂e) and a further shift towards LED-based revenues (85% to 90%).

Solar and Wind continued to be major contributors, consistent with previous years and the methodological emphasis on technology manufacturers. Power Generation also rose to the third-largest contributing sub-sector for the first time, reflecting increased renewable production by utilities, growth in distributed solar deployments (Sunrun), and higher sales of thermal hydrolysis pre-treatment systems (Cambi).

(function() {

var tag = document.createElement('script');

tag.src = "https://plausible.io/js/script.outbound-links.pageview-props.tagged-events.js";

tag.defer = true;

tag.setAttribute("data-domain", "dnbam.com");

var firstScriptTag = document.getElementsByTagName('script')[0];

firstScriptTag.parentNode.insertBefore(tag, firstScriptTag);

})();

Net Zero Engagement, a more focused and practical framework

Our net-zero assessment framework has been enhanced in close collaboration with the Responsible Investment team. The updates introduce clearer alignment with best-practice guidance, including the NZIF framework, and strengthened integration with DNB’s transition strategy.

The revised framework can now aggregate “degree of alignment” at both company and portfolio level, enabling progress to be tracked more systematically over time. While most data themes remain unchanged, we now incorporate performance elements such as three-year emissions trends and greater nuance around targets and scopes. This offers deeper insight into areas requiring further engagement.

Companies have responded positively to the more streamlined structure, particularly at a time when many have scaled back ESG reporting due to declining market sentiment. As in previous years, the annual heat map remains an important tool for visualising alignment and highlighting momentum.

The need for climate solution providers remain essential

Despite low sentiment around ESG and climate investing, the need for climate solution providers and enablers is stronger than ever.

Science indicates that a temporary overshoot of the 1.5°C limit in the early 2030s is now inevitable. Even a short-lived overshoot risks irreversible ecosystem damage and exposes billions of people to severe climate impacts. The need for both emissions avoidance and adaptation is therefore urgent.

At the same time, the clean energy transition continues to accelerate. Solar and wind are now the cheapest and fastest-growing sources of electricity in history, with almost all new global power-generation capacity in 2024 coming from renewables. Rising energy demand reinforces the critical role of renewables, electrification and energy efficiency, supported by modern grids and large-scale storage systems.

COP30 underscored a fragmented geopolitical landscape, delivering only modest progress. Countries reached a deal, but consensus was fragile, with China taking a low profile and petro-states slowing momentum. Fossil fuels were excluded from the final text, though a voluntary phaseout roadmap backed by 90 nations will proceed outside the COP process. Adaptation finance dominated outcomes, with a pledge to triple funding to 120USDbn annually by 2035, likely redirecting resources from mitigation. Trade tensions re-emerged, particularly around the EU Carbon Border Adjustment Mechanism (CBAM), and a dedicated 2028 review will assess trade’s role in climate policy. Forest protection advanced through Brazil’s new Tropical Forest Forever Facility, funded with USD 6.6 bn, though deforestation targets were omitted. Over 100 new NDCs indicate potential warming of 2.3–2.5 °C, supported by a voluntary “global implementation accelerator.”

Despite mixed progress, financial materiality of climate and nature risks continues to rise: 1) more countries are advancing fossil-fuel phase-out policies, albeit voluntarily, 2) carbon pricing mechanisms are expanding, 3) the costs of physical climate impacts (and investment in adaptation) are increasing, and 4) nature finance is now firmly embedded in the COP agenda.

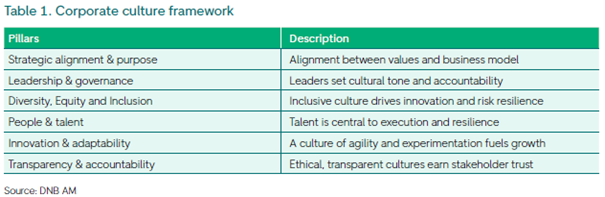

Corporate Culture, an under-analysed driver of long-term value creation

Corporate culture is a significant yet often under-examined contributor to long-term value creation. It influences talent retention, innovation, customer outcomes, risk management and financial performance. We view culture as a central component of competitive advantage, resilience and sustainability, and therefore an integral part of our investment process.

Examples of how culture shapes financial outcomes include stronger talent retention (reducing turnover costs), greater innovation capacity, more robust governance and risk management, broader and more inclusive decision-making, and higher productivity and safety performance.

To better assess these dynamics, we have developed a corporate-culture assessment framework drawing on internal experience, external research, sell-side insights and stakeholder engagement.

This year’s report also includes an initial assessment of Schneider Electric. While further refinement is ongoing, the overall directional view is consistent with our longstanding assessment of the company’s culture. Future updates will include more detailed company-level findings as the framework matures.

Final word

The 2024 DNB Renewable Energy PAE Report reaffirms the strength of our investment process in identifying climate solution providers and enablers. Even as methodologies evolve and data complexities increase, one conclusion remains clear - the portfolio potentially avoids more emissions than it generates. With strengthened frameworks for assessing net zero alignment and corporate culture, we are better equipped than ever to interpret these results and identify where the next opportunities for progress lie.