First Half of 2025: Strong Returns in the Nordic Bond Market

The second quarter has been dominated by a series of major international events, which have also impacted the Nordic bond market.

Nordic High Yield

The Nordic high yield market has performed quite well over the past few years.

The combination of relatively short interest rate duration (typically around 1 year) and moderate credit duration (typically around 2.5 years) has created decent returns.

At the same time we have seen an active Nordic high yield market with strong new issuance and a continued growth in outstanding volumes and number of issuers in the market. Actually, we have seen a market growth of more than 20% since 2021 whereas both the US and European high yield markets have become smaller since 2021.

Strong performance

Looking at the DNB High Yield Fund performance has been attractive relative to a broad European high yield benchmark, both on a shorter and a somewhat longer horizon.

Diversification benefits

The correlation between the return in the Nordic high yield fund and European high yield is clearly positive but there will still be diversification benefits as correlation is far from perfect. There will also be positive correlation with equity market returns as the high yield and equity markets will be influenced by the same risk factors, be it geopoliticial tensions or trade policies (tariffs), But again, correlation will be far from perfect.

Still higher credit-spreads than pre-april

Credit spreads in the Nordic high yield market widened in early April on the new proposed tariff regime from the US. As we saw some pullback and the start of negotiations concerning tariffs we have seen credit spreads turn around and come some of the way back but spreads are still around 70 basis points higher than pre-April.

Nordic HY: Higher spreads than rest of Europe

Measured by the DNB Carnegie high yield index Nordic credit spreads are at 477 basis points which is around 150 basis points above the spreads on the Bloomberg Pan-European benchmark at present. The typical picture is that Nordic high yield credit spreads are quite a bit above European/US high yield credit spreads.

This may partly be due to the fact that a substantial number of HY issuers in the Nordic region are unrated and also that the average size of companies and issues would be smaller then for European/US high yield.

The return over time indicates that investors are being adequately compensated for these risks.

After a period in which interest rate sensitive sectors, such as real estate and diversified financials, traded at elevated spread levels we have seen spreads for these sectors normalize as central banks started cutting interest rates. At present there is relatively little dispersion between credit spreads for different sectors.

Our philosophy is based on bottom up investment where we build the portfolio from the individual deals and where we strive to keep the portfolio well diversified over sectors and companies. Thus, we are not dependent on large volatility in spread development between different sectors.

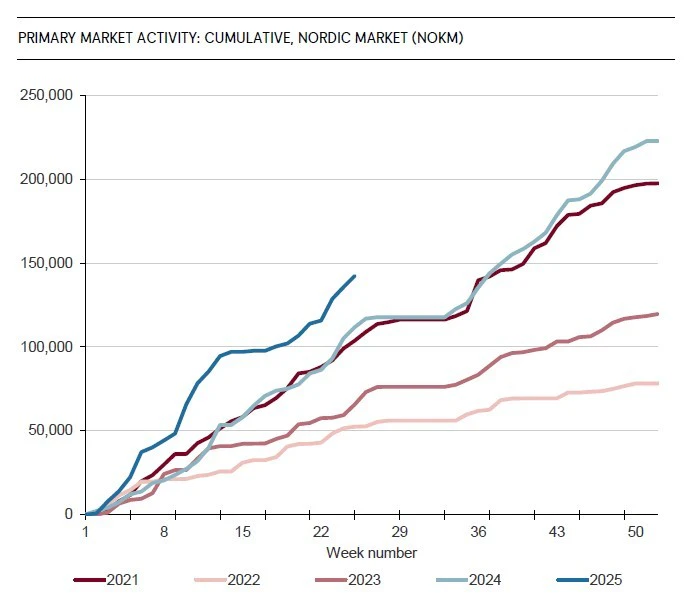

High activity in the Nordic Issuance market

The Nordic high yield market has been quite active so far in 2025 with a strong new issuance market and high liquidity in the secondary market. New issuance is on a path to a new record year after setting a record also in 2024.

This is in contrast to high yield markets in Europe and the US where outstanding volumes in the markets reached a top in 2021 and have been reduced since then. We also see the investor base for Nordic high yield becoming more international leading to increased liquidity in the secondary markets.