Published:

The DNB High Yield fund (Inst A NOK share class) returned 0,02% in August. As of September 10th the fund returned 6,07% to our investors which is fully in line with our expectations.

August performance +0,02% in NOK (Inst A NOK share class)

YTD return 6,07 % in NOK

EUR/NOK with strong movement

Svein Aage Aanes, Head of Fixed Income at DNB and Co-Portfolio manager of the High Yield fund, decided to launch a (Norway domiciled) HY fund in 2012. At this point in time DNB thought it might be a good idea to launch a dedicated High Yield fund as the Nordic HY market has grown over time. Today we think about the Nordic HY market as a fully established and well diversified market. Back in time the banks, brokers and market participants did their own credit research and every bond issued got a so called “shadow rating”.

Please find the development in EUR & NOK for other share classes below.

As many issuers are and were not willing to have a rating from an established rating agency we have now a situation where issuers with good credit qualities are still unrated. These companies are mostly recurring issuers and often strong brand names in the Nordic universe. This is a good opportunity for investors to buy a reasonable credit quality at higher spreads compared to rated issues in other markets, for example EU and US High Yield.

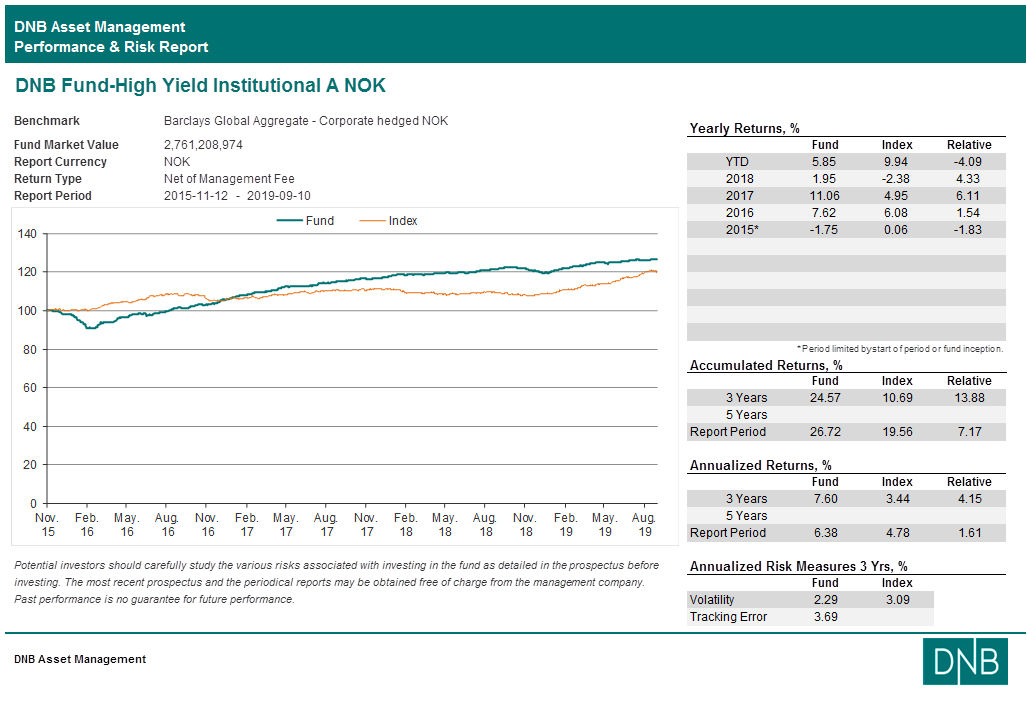

We launched the Luxembourg domiciled fund in November 2015 and gained a lot of attraction from our international clients. The Luxembourg domiciled fund has grown to 326m EUR and shows a very attractive track record. Since inception investors earned 6,38% annually in combination with a relatively low 3Y-volatility of 2,29%.

Please find details below:

As we are operating in a more and more diversified market which is still growing, we are not afraid of not finding enough interesting bonds for our strategies. At the moment the 71 bn. EUR sized market has a share of 8% in oil and gas service companies. We expect this part of the market to reduce to 5% over time.

Which brings us to the oil price and the development of Nordic currencies.

The oil price decreased from USD 65 to USD 59/bbl. in August. The oil price decrease followed mainly from increased concern about global growth and oil demand going forward. On the supply side we now see the number of oil rigs operating in the US shale oil industry dropping.

Both the SEK and the NOK weakened in trade weighted terms in August. Both currencies seem to be negatively influenced by trade and growth worries in the present market climate as investors focus on the larger safe haven currencies.

During August the Euro strengthened 2,54% against the Norwegian currency. But: YTD EUR/NOK is nearly unchanged with -0,4%.

I must admit I am surprised about the weakness of the Nordic currencies and in particular about the weakness of the Norwegian currency. It surprises me a bit that the recovery in oil did not strengthen the Norwegian currency as much as expected, but a drop in the oil price and growth concerns let the currency drop like a stone end of July, beginning of August.

We observe this development closely.

Nordic economies

Macroeconomic developments in Norway still point towards GDP growth in 2019 in the interval 2.7-3.0%. The labor market is strong with unemployment just over 2%, although the fall in unemployment has levelled off. Based on Norwegian developments in isolation we would be on a path for a very likely rate hike from the central bank rate in September. However, global developments in August pull in the opposite direction with an intensification of the trade war, continued relatively weak macroeconomic data and a marked fall in interest rates. At present we see a potential rate hike in September from Norges Bank as a 50-50 probability. At any rate, we do not see any further rate hikes in this cycle from the central bank after the September meeting.

The Swedish economy continues to cool off with unemployment increasing a bit and the manufacturing sector feeling the effects of the global contraction in trade volumes. We expect this development to continue and we do not see any further rate hikes from the Swedish central bank. If global conditions continue to deteriorate we could end up seeing rate cuts from the Riksbank in 2020.

Outlook for the fund

The investor base for Nordic high yield bonds has grown lately. At the same time the investment universe has grown. Compared to European high yield, we find Nordic spreads attractive and view risk return as good.

One last remark:

Please keep in mind that DNB High Yield is an actively managed fund with a competitive cost structure for you, our dear clients. Spreads are still on attractive levels but one day we might see a global sell-off in risk assets. In this case I would feel more comfortable in an active fund where the portfolio manager is looking for relative value whereas passive investments are probably stuck in a situation forced to sell high quality bonds at lower prices.

Disclaimer: Nothing contained on this website constitutes investment advice, or other advice, nor is anything on this website a recommendation to invest in our Funds, any security, or any other instrument. The funds mentioned may not be available in the markets you represent. The information on this blog is posted solely on the basis of sharing insight to make our readers capable of making their own investment decisions. Should you have any queries about the investment funds or markets referred to on this website, you should contact your financial adviser.

Last updated:

Share: