Published:

Aside from the obvious questions concerning the rate of spread and mortality of the virus, financial markets have been preoccupied with estimating the economic fallout from the virus and from the measures implemented to contain it.

By now it is received wisdom that there will be a major short term impact on growth in China and major parts of Asia. This follows directly from the shut-down of economic activity in large parts of China and travel restrictions within China, and also between China and a number of other countries. There is also a growing realization that global value chains will be impacted in many industries, most recently made clear by the profit warning from Apple for Q1 2020. Other industries, such as automobiles and airlines will also be impacted.

The financial markets have been remarkably stable

Relative to the massive media and analyst coverage of the effects of the virus financial markets have been remarkably stable. Whether we look at equity or credit markets the main observation is that market impacts so far have been quite modest.

Investment Grade credit spreads in Europe and the US:

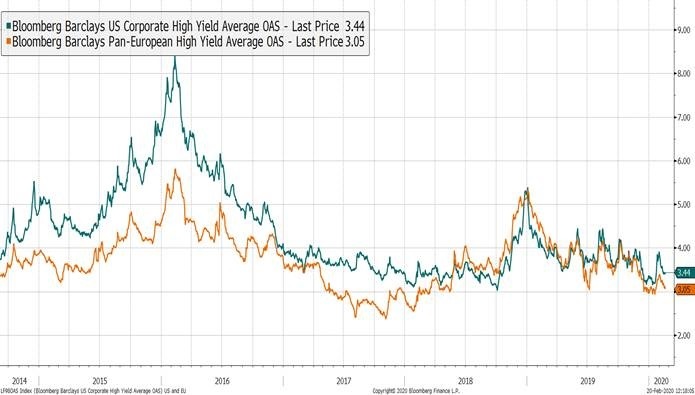

High Yield credit spreads in Europe and the US:

Equity markets (normalized from 30.09.2019)

As the illustrations show there was some initial short-lived volatility in the various markets in the second half of January. Since then the markets have rallied and even the Chinese equity market has now returned to close to previous highs.

So what is going on?

It seems that whereas ‘everybody’ agrees that the growth impact will be quite massive in Q1 2020, there is also agreement that the virus will be contained and that much of the growth reduction in Q1 will be made up for by higher growth for the remainder of the year and into 2021. Thus, analysts are typically reducing their global growth estimates for 2020 by a couple of tenths of a percentage point.

Based on previous experiences with virus outbreaks this null hypothesis seems eminently reasonable, although it is way too early to conclude how this situation will pan out. Among other things, although we can point to what happened during and after the SARS epidemic, we actually have little experience with this kind of virus outbreak in a world in which China’s importance for global production and value chains is at today’s unprecedented level. Thus, there are clearly still risks emanating from the unresolved COVID-19 situation.

The Nordic countries are well placed to combat potential global setbacks from COVID-19

Given that global risk markets so far have not been strongly affected by the COVID-19 virus it is perhaps not a surprise that the Nordic high yield markets have not been strongly affected either. The direct effects of the virus situation in the Nordics is so far very limited. At present there are two confirmed cases of the virus in Nordic countries (1 in Sweden and 1 in Finland). The tourist industry has experienced reductions in the number of travelers, particularly from China. But this is not a very busy time of the year for the tourist industry so the effects are close to negligible in a macro sense.

Clearly some companies in the Nordic countries with a global business model will experience potential indirect effects through reduced export volumes or interrupted value chains. For instance, this could be the case for some of the companies in the shipping sector. On the other hand, there are many companies with more local business models that are unlikely to experience even temporary setbacks.

We share the basic hypothesis that COVID-19 will mainly be a temporary phenomenon and that it is not likely that the situation will have long-lasting effects on global growth and company earnings. But it is interesting to reflect on what would happen if the situation were to develop into a truly global pandemic with more pronounced and longer lasting effects on global growth. In this scenario we think that the Nordic countries would fare relatively well. It is important to stress the word relative here as we would not argue that the Nordic high yield market could go completely against the stream in this scenario, which would likely entail a sell-off of risk assets.

We are quite far away from the center of the outbreak

We do believe however, that the Nordic countries and the Nordic high yield market are quite well placed to handle this kind of situation. For one thing, we are quite far away from the center of the outbreak. Simple geography indicates that the Nordic economies would not experience the hardest direct hits in the form of the number of COVID-19 cases.

In addition, a high level of trust in authorities (also medical authorities) and very advanced and wide ranging health systems create a strong base from which to fight a virus outbreak. It is highly unlikely that a virus outbreak in the Nordic countries would lead to the massive measures we have seen in China and some other countries – such as the closing of workplaces and schools and heavy travel restrictions.

In a closely interlinked global economy the Nordic countries would also feel the effects of slower global growth in this scenario. Luckily, the Nordic countries still have a lot of fiscal firepower and a demonstrated willingness to employ that firepower to fight potential recessions. So also on this score we think the Nordic countries and the Nordic high yield market should fare well in relative terms in this scenario.

Disclaimer: Nothing contained on this website constitutes investment advice, or other advice, nor is anything on this website a recommendation to invest in our Funds, any security, or any other instrument. The funds mentioned may not be available in the markets you represent. The information on this blog is posted solely on the basis of sharing insight to make our readers capable of making their own investment decisions. Should you have any queries about the investment funds or markets referred to on this website, you should contact your financial adviser.

Last updated:

Share: