Published:

This is part one in a three part mini-series on the topic of systematic trend investing. In part two we will look closer at what a trend is and how we can identify one. In the last part we will look at how we can design a systematic trend strategy, followed by a practical example.

When the price in a market is moving in one overall direction, such as up or down, that is called a trend.

Traders in the stock and commodity markets have tried to find ways to capture trend profits for at least 200 years.

What’s in a name? That which we call a rose By any other name would smell as sweet

“What’s in a name?”

Trend investing comes in many shapes and forms and is referred to by many names in the academic literature. From time-series momentum (TSM), also known as trend momentum or trend-following, and cross-sectional momentum (CSM) that is often referred to as the momentum factor, to managed futures and CTA.

Time-series momentum is an absolute strategy that looks at the price trends of each asset individually. If the recent price has gone up, then we take a long position, if it has gone down we take a short position. We can compare this to the traditional (cross-sectional) momentum factor that ranks assets on a relative basis, and goes long on the top-most percentile and short on the bottom.

If the momentum strategy is realized using futures instruments, it is usually referred to as a “managed futures strategy” or a CTA, short for “Commodity Trading Advisor”[1]. In the context of trend investing, the acronym CTA is commonly used for asset managers following investment strategies utilizing futures contracts on a wide variety of asset classes.

The history of trend investing

The idea of trend investing runs back at least to the 18th century where, according to the book “The Great Metropolis, Volume 2” from 1838, David Ricardo stated to “Cut short your losses” and “Let your profits run on”. Said another way; trend investing.

Another central figure in the early history of trend investing was Jesse Livermore (1877 - 1940), possibly the most famous trader in history, that supposedly should have said “… the big money [is] not in the individual fluctuations but in the main movements …”.

Cut short your losses; Let your profits run on

All trend investing boils down to two basic steps

All trend investing strategies have in common that they try to isolate and extract profit from trends. We can simplify this process down to two basic steps:

- First, use historical price movements for determining if there currently is a trend.

- Then, find the direction and take positions accordingly.

While a traditional manager will use discretion for selecting the positions, a systematic trend strategy will rely on a set of pre-defined quantitative rules and methods executed under the supervision of a portfolio manager.

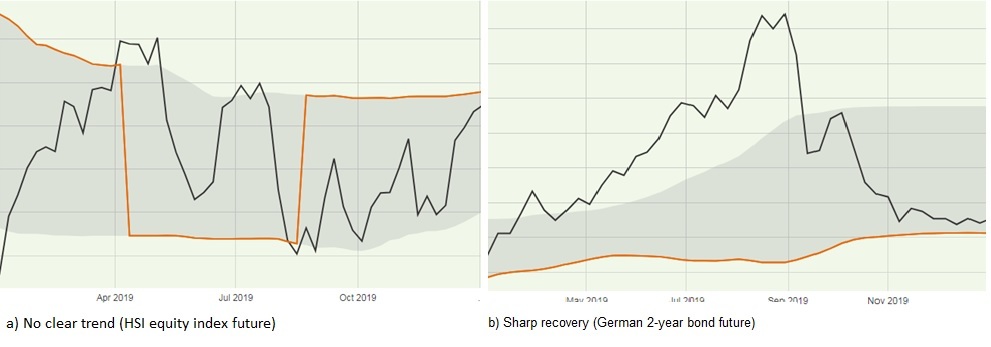

Trend strategies tend to underperform during market turning-points

Due to their reactive nature trend strategies tend to underperform during market turning-points, especially when there is a sharp recovery. They also tend to suffer and show tail-risk and negative skewness when there is no clear trend, or during mean reverting markets when trend detection is wrongly identified.

In a diversified trend strategy, the asset classes will typically experience different timing of turning points, and will also have different timing for the individual markets within each asset class, which contribute to offset these risk characteristics.

Trend investing complements traditional portfolio management

Averaged over time, trend investing strategies have shown low to negative correlation with other asset classes, though they do have time-varying market exposure and periods with significant market beta. They have historically also offered low to negative correlation during market corrections.

Traditional asset portfolios and trend strategies complete each other.

Trend strategies have experienced limited drawdowns compared to equivalent long-only portfolios, and have also delivered strong performance during market crises, as they can be both long- and short positioned.

These return/risk characteristics make trend investing efficient overlay strategies to traditional asset portfolios as the strategies complete each other.

This is the first in a three part mini-series on the topic of systematic trend investing. The next part is: Has the sun set for trend investing strategies?

[1] CTA is a regulatory term used for individuals or organizations that provide advice or services related to futures contracts.

[2] With the technical analysis pioneers William Dunnigan (died 1957) and his publication “Trading with the Trend” from 1934, and the better known Richard Donchian (1905 - 1993) with his article “Trend-Following Methods in Commodity Price Analysis”

[3]Examples are Jegadeesh and Titman (1993) in equity markets, Asness, Moskowitz and Pedersen (2013) in fixed income markets, Erb and Harvey (2006) in commodity markets, and Burnside, Eichenbaum and Rebelo (2011) in currency markets.

Disclaimer: Nothing contained on this website constitutes investment advice, or other advice, nor is anything on this website a recommendation to invest in our Funds, any security, or any other instrument. The funds mentioned may not be available in the markets you represent. The information on this blog is posted solely on the basis of sharing insight to make our readers capable of making their own investment decisions. Should you have any queries about the investment funds or markets referred to on this website, you should contact your financial adviser.

Last updated:

Share: